Skip to main content

Skip to main content

Laos: The Window No One Is Watching Yet

Laos exports 50,000 tonnes of coffee annually — from a single plateau — and the two founder-owned brands that built the market are both in their seventies, both transitioning to daughters, and both invisible to every major institutional database on earth. The entire private sector was built in fifteen years. It is now aging out simultaneously.

Bolaven Plateau, Luang Prabang, Phongsali: Laos's three founding geographies

The single-plateau generation, 1986–2024

The two founders who built Laos’s coffee export industry have spent a combined 60-plus years on the Bolaven Plateau, trained their daughters to take over, and remained entirely invisible to every investment database on earth. One of them — Sinouk Sisombat, who returned from France to found Laos’s first branded coffee company in 1994 — is estimated to be in his mid-seventies to early eighties. The other, Leuang Litdang of Dao-Heuang Group, built the largest private company in Laos from an import-export startup. She is approximately 73. Both succession transitions are actively underway. Neither appears in PitchBook, Bloomberg, or any Southeast Asia consumer sector report.

This is the peculiar condition of Laos’s private consumer economy: it was built by a generation of founders who were, by any reasonable measure, extraordinary — and it has been documented almost entirely in Thai and Lao, in trade bulletins that no institutional investor reads, in a country that international capital has rarely bothered to examine. The New Economic Mechanism reforms of 1986 created the space for private enterprise. The 1997 Asian crisis tested it brutally. COVID-19 nearly ended it. And the sovereign debt crisis of 2022–2024 — 88.5% kip depreciation, inflation at 41.3% — is now doing something the earlier shocks did not: forcing premature exits from founders who have run out of time to wait.

The compressed wave

Laos's two largest coffee exporters have operated for a combined 60-plus years, trained family successors, and achieved global distribution — yet neither appears in PitchBook, Bloomberg, or any Southeast Asia consumer sector report.

Mongolia’s private sector was created in roughly two to three years following the 1990 democratic revolution. This earned it the most extreme “compressed wave” designation in Brandmine’s succession research. Laos is different in degree but similar in kind: the entire NEM reform arc from 1986 to 2005 — nineteen years — created a founder cohort from scratch. There was no pre-existing capitalist class, no merchant family tradition, no accumulated institutional knowledge about how to build, transfer, or sell a private business. Every founder learned from first principles.

The founders who stepped in — often returning diaspora members, former civil servants, or small traders — had no templates, no mentors, and no institutional infrastructure. They built on personal relationships, family labour, and trade credit. Their businesses are, by design, inseparable from their personalities.

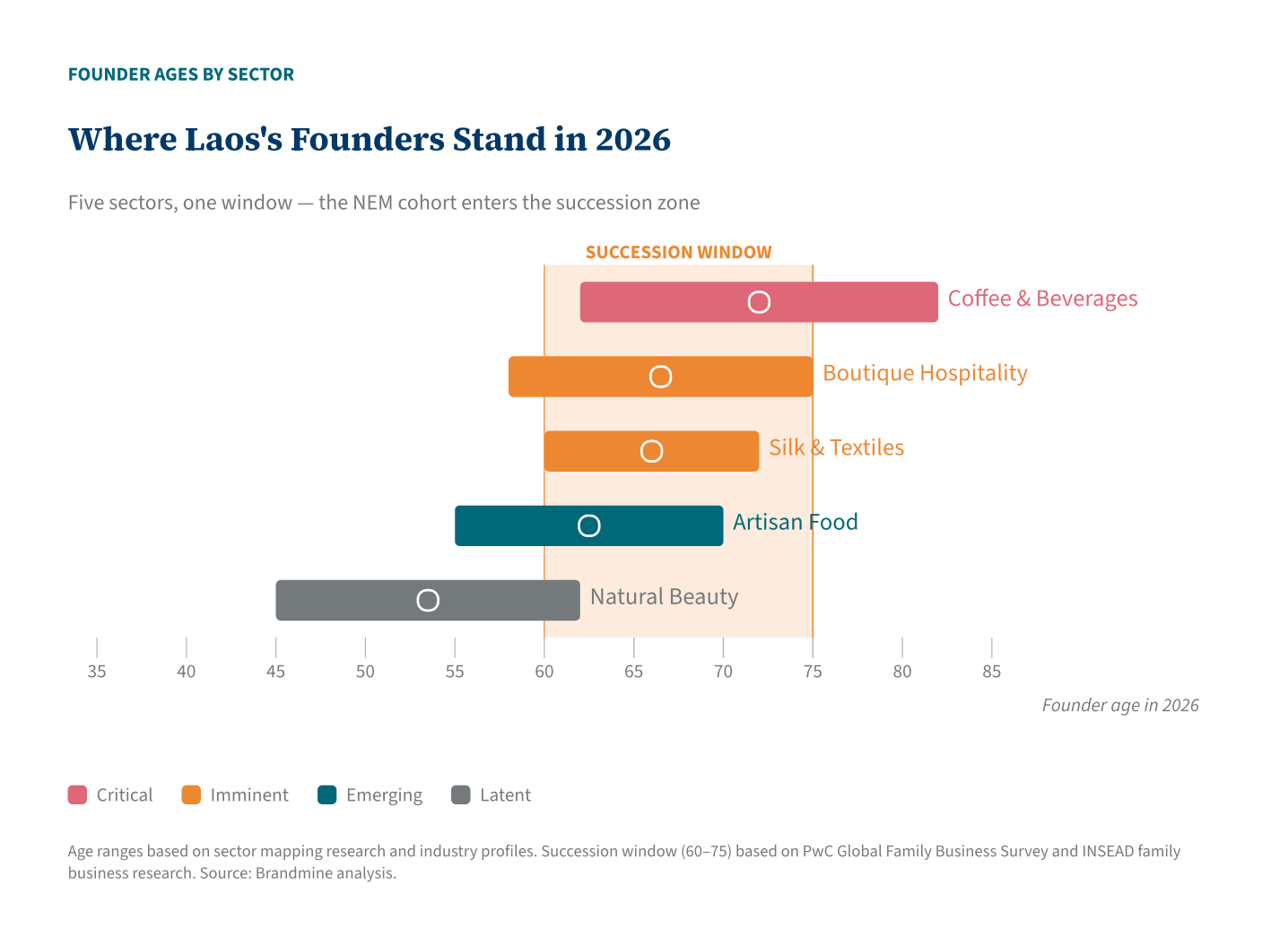

The founder age bands by sector reflect the wave’s timing. The oldest cohort — coffee and some hospitality — launched in the late 1980s and early 1990s, when founding conditions were most chaotic and founding risk was highest. These founders are now in their late sixties to early eighties. The Imminent cohort — the rest of hospitality and silk weaving — followed in the mid-1990s after ASEAN accession reduced some of the regulatory uncertainty. They are now in their early to mid-sixties. A younger Emerging cohort, primarily in artisan food, is in its mid-fifties to early seventies. Natural beauty remains effectively pre-succession — the sector never consolidated beyond micro-artisan scale.

The Laos-China Railway, which opened in December 2021, is reshaping the terrain even as the succession clock runs. Chinese tourist arrivals grew 63% in 2024 alone; international hotel chains are opening in Vientiane for the first time. Brands positioned to serve Chinese visitors and export across the rail corridor have a structural tailwind that domestically-focused founders do not. The wave is not moving uniformly — it is bifurcating between those with dollar revenues and those trapped in kip.

One complication specific to Laos compounds all of this: it is the most opaque market in Southeast Asia for English-language research. The Thai-language press — Bangkok Post, The Nation, Thai business publications — covers Laos’s coffee and tourism sectors with considerably more depth than any English-language source, because Thailand is Laos’s largest trading partner and Thai capital has been present in the country for decades. Lao-language directories, LNCCI registry records, and sector-specific trade associations publish material that has never been translated or synthesised for international audiences. This is not a minor gap. The two most thoroughly documented founders in Laos’s consumer brand ecosystem — Leuang Litdang of Dao-Heuang and Sinouk Sisombat of Sinouk Coffee — have biographical material in Thai, French, and Lao that required years to surface, and which no investment database has ever aggregated.

Who is in the window now

Coffee & specialty beverages — two confirmed targets, Critical urgency. The Bolaven Plateau is among Southeast Asia’s most distinctive single-origin coffee geographies: high altitude, volcanic soil, reliable rainfall, a registered Geographical Indication, and $100M+ in annual exports. Dao-Heuang Group and Sinouk Coffee built this market from nothing. Both founders are in their seventies; both are actively transitioning to daughters (Boonheuang Litdang at Dao-Heuang, Sirina Sisombat-Hervy at Sinouk). The succession processes are documented, multi-year, and — critically — already partially public in Thai and English business press. The NDD material exists. It has simply never been assembled. Beyond these two anchors, the Bolaven Plateau has a secondary tier of smaller roasters and plantation brands whose founders may be invisible even to Thai media. Coffee is the entry point. No other sector in Laos offers this combination of confirmed brands, documented founders, and active succession events.

Boutique hospitality — five to twelve candidates, Imminent urgency. Laos’s UNESCO heritage status (Luang Prabang, Wat Phou) created an artisan hospitality ecosystem that could not have existed in any less distinctive country. The Satri House ecosystem — Satri House hotel, Luang Say Mekong Cruises, Luang Say Lodge, four additional properties — was built by Lamphoune Voravongsa, a Lao woman who returned from France after thirty years in exile and named her hotel “House of Women.” Luang Say Cruises shut down entirely for five years during COVID, underwent full renovation, and reopened in 2025, calling it “a rebirth.” The Souphattra Hotels/Lao Derm Group offers a multi-city portfolio that likely clears the $5M threshold but whose founder identities remain opaque to English-language research. The COVID crisis is the defining event for every Luang Prabang brand — 80% of businesses closed, 70% of tourism workers lost income. The brands that survived have documented stories of what founders do when everything stops. A Sector Spotlight on Lao boutique hospitality is on Brandmine’s research roadmap.

Silk & traditional textiles — three to eight brands, Imminent urgency. Laos has a weaving tradition that stretches back centuries, a UNESCO-recognised practitioner (Kongthong Nanthavongdouangsy of Phaeng Mai Gallery, prize 1992), and an expatriate founder (Carol Cassidy of Lao Textiles) whose 35-plus years in Laos have generated more published NDD material than any Lao-national brand outside coffee. The challenge is revenue: most documented brands appear to operate at the $1–3M range, below the standard $5M Brandmine threshold. The case for a Laos-specific threshold recalibration — acknowledging that $5M represents an entirely different achievement in a $19.5B economy than in India or Indonesia — is strongest here. Sector scoping recommended before committing research resources.

Artisan food & condiments — two to five candidates, Emerging urgency. Padaek (fermented fish paste), Lao chili sauces, and jungle honey have been household staples for generations. What they have not been, until very recently, is branded consumer products with founders, stories, or export ambitions. The one identified operation with brand intent — Xaobangroup — is Dutch-Lao in origin and sub-$500K in revenue. What the Lao-language LNCCI directories might reveal is unknown; the sector is opaque to English research. The founding cohort, if it exists at the commercial level, is likely in the Emerging urgency band — established enough to have a brand, young enough to still be building.

Natural beauty & wellness — Latent urgency. The botanical ingredient base exists: Mekong herbs, highland plants, and traditional Lao medicinal knowledge. What does not yet exist is a founder-owned consumer brand that has consolidated this raw material into an internationally-marketable product at commercial scale. Eighty percent of cosmetics sold in Laos are imported from Thailand. The micro-artisan brands that have emerged (Saoban, Lao Natural) are sub-$500K and founder-anonymous. This sector is worth monitoring — the ingredient story is real and the Chinese tourist market will eventually create demand — but it is not yet a succession intelligence target.

Why Laos reads differently

Every compressed founding wave produces a specific kind of succession crisis. In Mongolia, the wave was so short — two to three years — that an entire private sector entered the succession window almost simultaneously, with no generational stagger to allow earlier successions to model the path for later ones. In Laos, the wave was slightly longer — roughly fifteen years — but the outcome is structurally similar. The founding generation all learned from scratch. It all started building at the same time. And it will all face succession pressure within a narrow window.

What makes Laos distinct is not the wave’s compression but its context. Theravada Buddhist cultural norms — the same framework that governs daily life throughout the country — make succession planning feel inauspicious. To formally prepare for one’s own exit is to acknowledge mortality; to transfer a business to a child while still alive is to diminish one’s own standing. This is not a marginal consideration. It is a structural cultural barrier that suppresses succession planning across the entire founder cohort, regardless of age or business size.

The institutional gap compounds the cultural barrier. There are no PE firms in Laos specifically targeting founder-owned consumer brands. The Lao National Chamber of Commerce and Industry (LNCCI) tracks registered businesses but has no succession facilitation function. No university offers family business governance curriculum. The two founders who have managed the most visible succession processes — Leuang Litdang and Sinouk Sisombat — did so through family mechanisms (bringing in daughters over a decade or more), not institutional frameworks.

Dao-Heuang’s trajectory is instructive. Boonheuang Litdang joined the company roughly twelve years ago and has been described as leading a “gradual management transition.” Her brother Howie manages the hotel business. Multiple children occupy leadership roles. This is what structured succession looks like in Laos: not a formal process, not a PE-mediated transaction, but a family absorption of management authority across a decade. It works — when there are willing heirs and a founder patient enough to share control. It does not work when the founder cannot share control, when the heirs are uninterested, or when the kip crisis forces the exit timeline forward before the family mechanism is ready.

Not every NEM-era founder has a Boonheuang or a Sirina. Most founder-owned businesses in Laos have no documented heir, no succession framework, and no institutional infrastructure. In a market where private equity essentially does not exist, the default outcome is not acquisition at fair value — it is premature wind-down or distress transfer. The succession infrastructure that would allow these businesses to transact appropriately does not exist.

The window and what it means

The kip crisis has created two Laoses for founder-owned brands. For coffee and boutique hospitality — both earning revenues substantially in dollars from export and foreign tourism — the depreciation has been painful but survivable. Dollar revenues, kip costs. The real value of the business in acquisition terms has actually increased for a foreign buyer. For domestically-focused brands — artisan food, textiles sold to local markets, beauty products priced in kip — the crisis has destroyed balance sheets and accelerated the timeline to exit.

This bifurcation matters because it is happening now. A founder who might have held on for another five years before beginning a serious succession conversation has been forced by the monetary reality to consider options sooner. A brand that might have been worth $3M in a calm market is being priced at distress valuations. The intelligence window — the period during which these founders are accessible, their stories documentable, their brands assessable — is not a future event. It is a present condition that is actively closing.

The China-Laos Railway adds a third dimension. Chinese acquirers and investors are arriving in Laos in numbers that no previous inbound capital flow has matched. They are looking at hospitality, at agriculture, at the food supply chain. They do not arrive as succession intelligence specialists. But they arrive with capital and with interest — which means the most commercially-attractive founder-owned brands in coffee and hospitality are, for the first time, being seen by potential buyers who have the means to act.

North of the coffee plateau, in Phongsali Province, ancient tea trees estimated at 400–800 years old supply raw maocha to Chinese buyers — a GI modelled on the Bolaven coffee registration is under development, but no Lao-owned brand has yet emerged. The value is being extracted; the brand equity is not.

The data on Dao-Heuang, Sinouk, Satri House, and Luang Say exists — it is in Thai business press, in UNESCO documentation, in trade association records, in founder interviews that have never been synthesised into a brief that an investor can act on.

Laos’s founders built for decades in a market that institutional capital never thought to examine. The two women who anchored the coffee sector did so through the Asian crisis, through the kip crises, and through a border closure that lasted two and a half years. Their daughters — Boonheuang Litdang and Sirina Sisombat-Hervy — are completing the transfer in Thai and Lao trade press that no PitchBook analyst reads. The railway brings Chinese acquirers to Vientiane with capital and without context. Whoever documents the Bolaven Plateau first will set the terms for everyone who arrives after.